Feels like 2026 just started and we're already staring at H2. AI still got a seat in basically every portfolio.

TradFi is still throwing stupid money at AI infra. So crypto continues to have a lot of room to grow, but where does crypto have a real wedge instead of just borrowing Nvidia’s narrative?

I only focus on real tech coins with catalysts heading into H2 2026.

1/ AI agent utility ramp

Agents are the easiest narrative for CT to understand because they already look like onchain behavior.

The froth died, and now the surviving names need to prove real agent payments, real launchpad revenue, real trading flow, and real wallet usage.

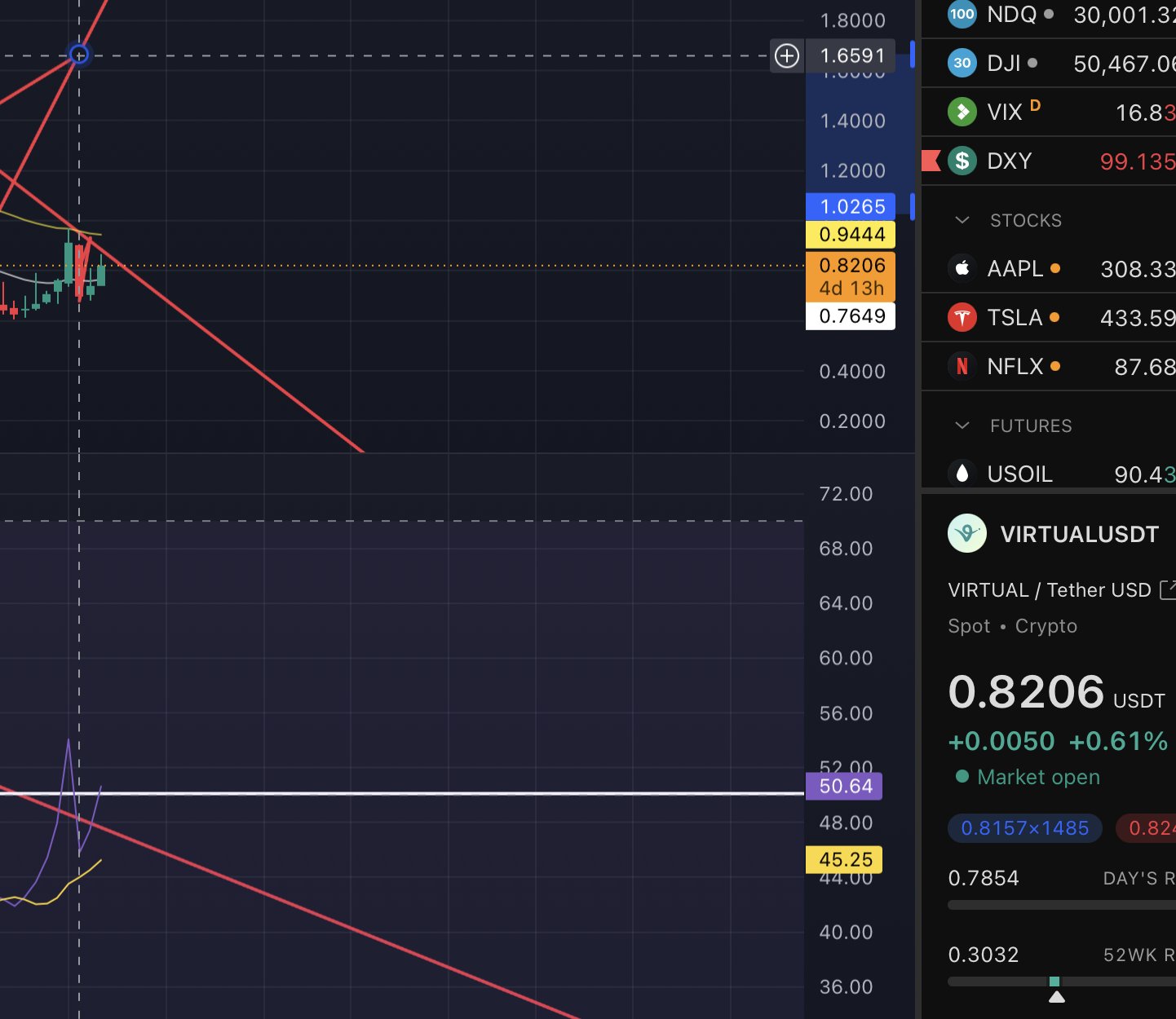

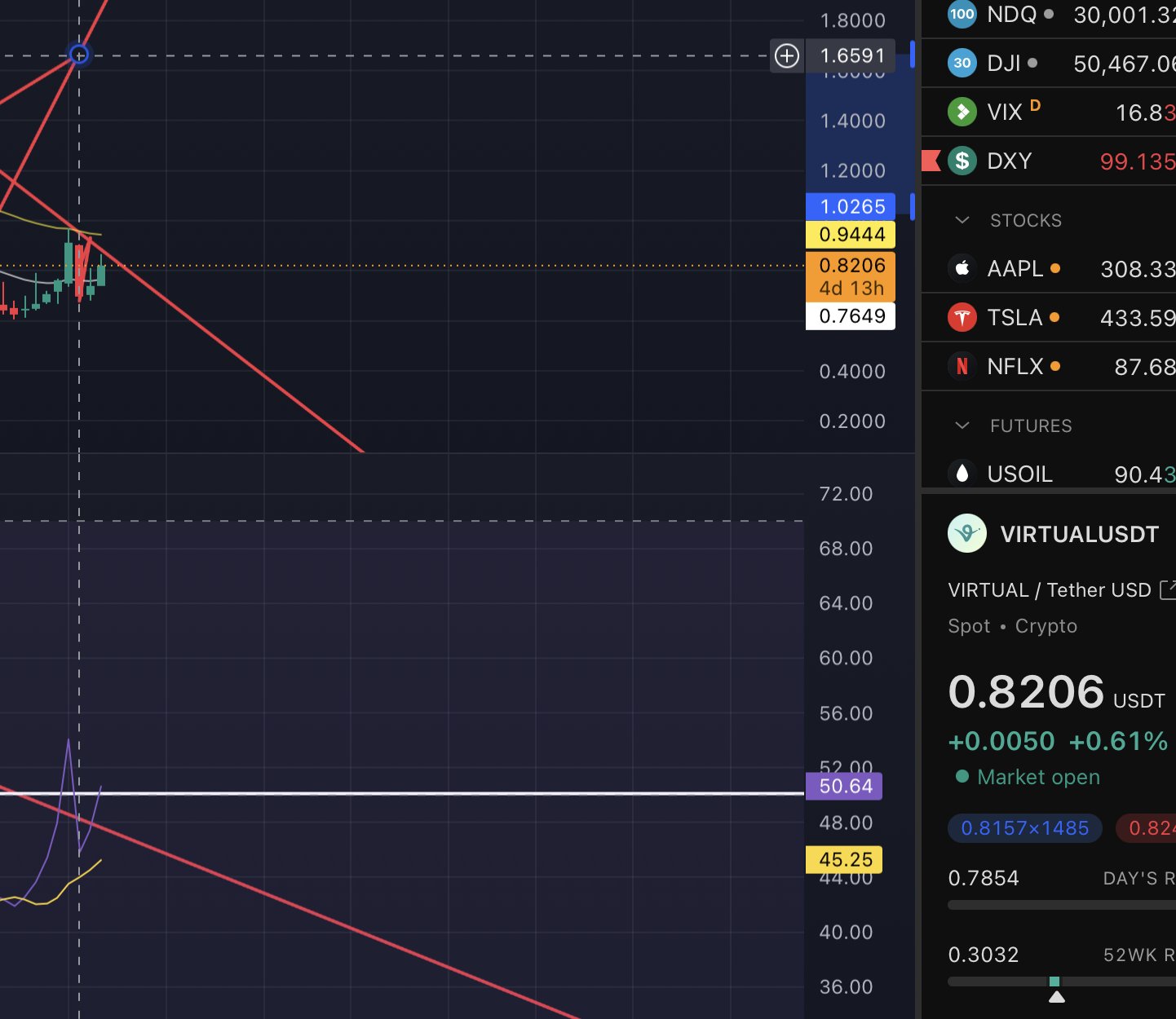

$VIRTUAL: ACP v2, ERC-8183, Revenue Network, and still the index bet on agent commerce and tokenized AI workers.

$BNKR: already doing more launchpad volume than Virtuals and controlling 67% market share on Base. Every AI launch on Base routes value to $BNKR.

$SERV : building full-stack agent startup rails with BRAID, no-code tools, SDKs, staking, launch payments, and buyback/burn mechanics, while already pointing at UAE government usage.

2/ DePIN supply explosion from consumer hardware and robotics

The next AI bottleneck is real-world data, robot data, bandwidth, machine identity, and eventually robots paying each other for skills, maps, energy, and maintenance.

Tesla wants 50,000 Optimus units by the end of 2026, Figure is already inside BMW, 1X is shipping NEO, and Unitree keeps pushing cheap robots into the market.

$GRASS: turning idle bandwidth into AI fuel with 2.5M+ active nodes and $33M verified revenue. Season 2 is the big H2 event with a 170M GRASS distribution.

$PEAQ: machine economy L1 with 3M+ machines, 60+ DePIN apps, 20+ industries, and 1.7B+ PEAQ staked.

$DEUS: the most direct retail wrapper for private robotics exposure, with treasury exposure to Apptronik, Figure AI, 1X, Agility, Neura, and Robotico.

$ROBO: building identity, coordination, and payment rails for robots through OM1 and crypto wallets for machines.

$CODEC: operator execution rails for robotics and AI agents. Just shipped SimArena to train robots directly in the browser.

3/ Privacy AI

Nobody serious wants their agent leaking prompts, customer data, trading logic, or source code into some random model endpoint forever.

$VVV: 2M+ users, 1M+ API calls/day, and 50k–150k DAU. People will continue staking $VVV for inference capacity. DIEM turns compute into a weird perpetual API credit.

$NEAR: NEAR AI Cloud, Private Chat, IronClaw, Confidential Intents, chain abstraction, and Intents all stack together. $19B cumulative Intents volume, $32M fees, and $68M shielded volume.

$NIL: privacy compute underdog with nilDB, nilAI, and nilCC, plus 130M+ privacy-preserved data points processed.

$NOCK: ZK proof-of-work L1 where miners generate STARK proofs over NockVM, and the cuPoW thesis lets MatMul work connect directly to AI workloads.

4/ AI data and compute

Hyperscalers are fighting for power, HBM, CoWoS, data centers, and GPU clusters. Half of the US data centers planned for 2026 are facing delays from land, energy, and permitting constraints.

Real decentralized compute, model, inference, and data marketplaces look like shadow supply.

$TAO: still the main play on decentralized intelligence with 128 active subnets, ~70% of supply staked, and the $TAO ETF narrative coming.

$PRL: trying to turn AI computation itself into network security through Proof of Useful Work. Generates zk proofs through Plonky2 and secures the chain while producing compute that can be reused for inference.

$RENDER: GPU coordination at scale. 63M+ rendered frames and thousands of active GPU nodes. Started with rendering but increasingly sits inside the broader AI workload conversation.

$AKT: decentralized cloud markets. Record $5M Q1 compute spend, 120B tokens processed in April, and growing AI demand looking for cheaper alternatives to hyperscalers.

Not every AI headline will need a ticker. The market probably rewards the ones with revenue, tech, and utility rather than vapor.

Virtual Protocol (VIRTUAL)

Virtual Protocol (VIRTUAL)