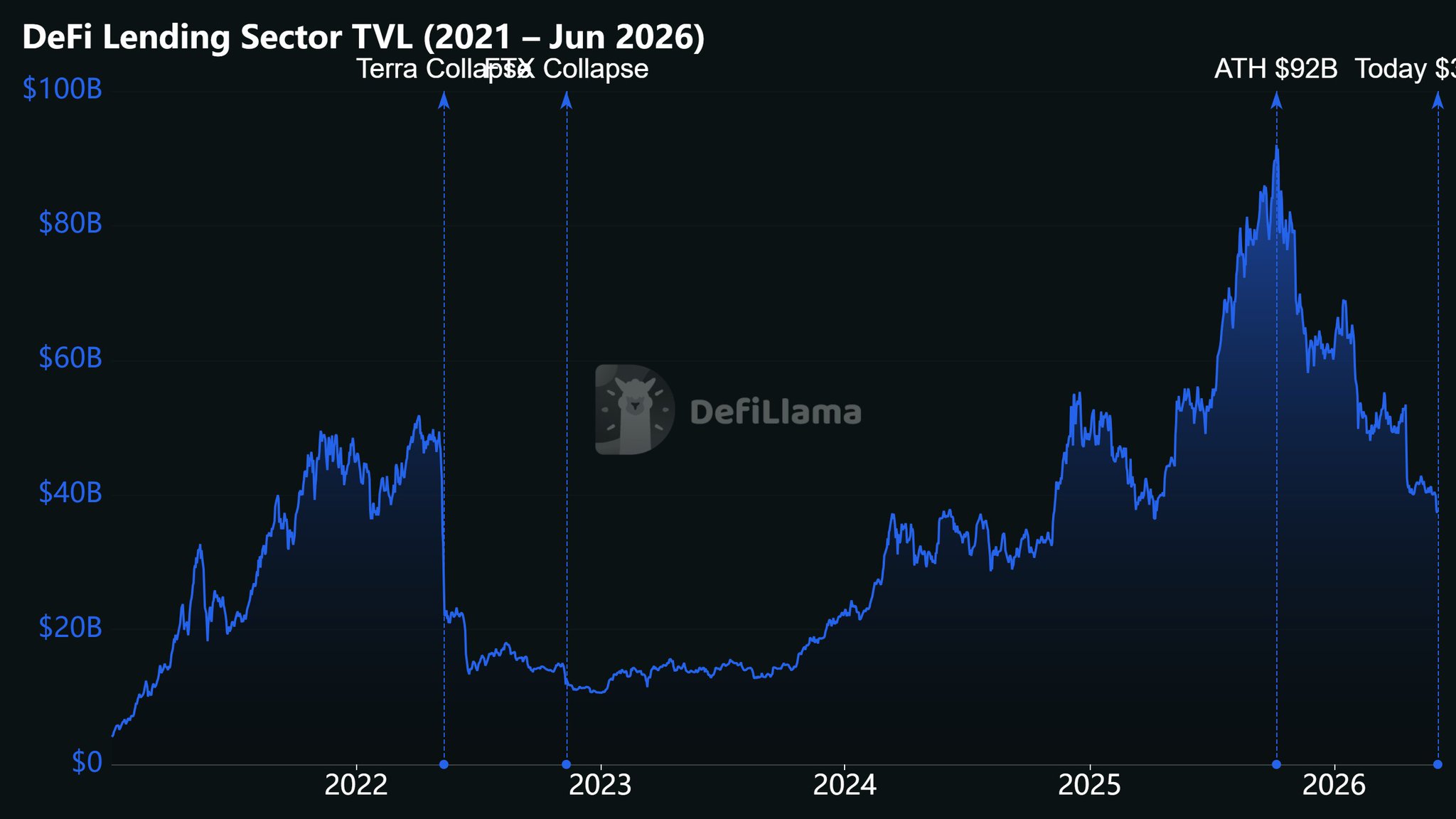

Lending has remained DeFi’s core credit layer since 2021.

Its TVL reached a new peak in October 2025 as newer models and protocols continued to emerge.

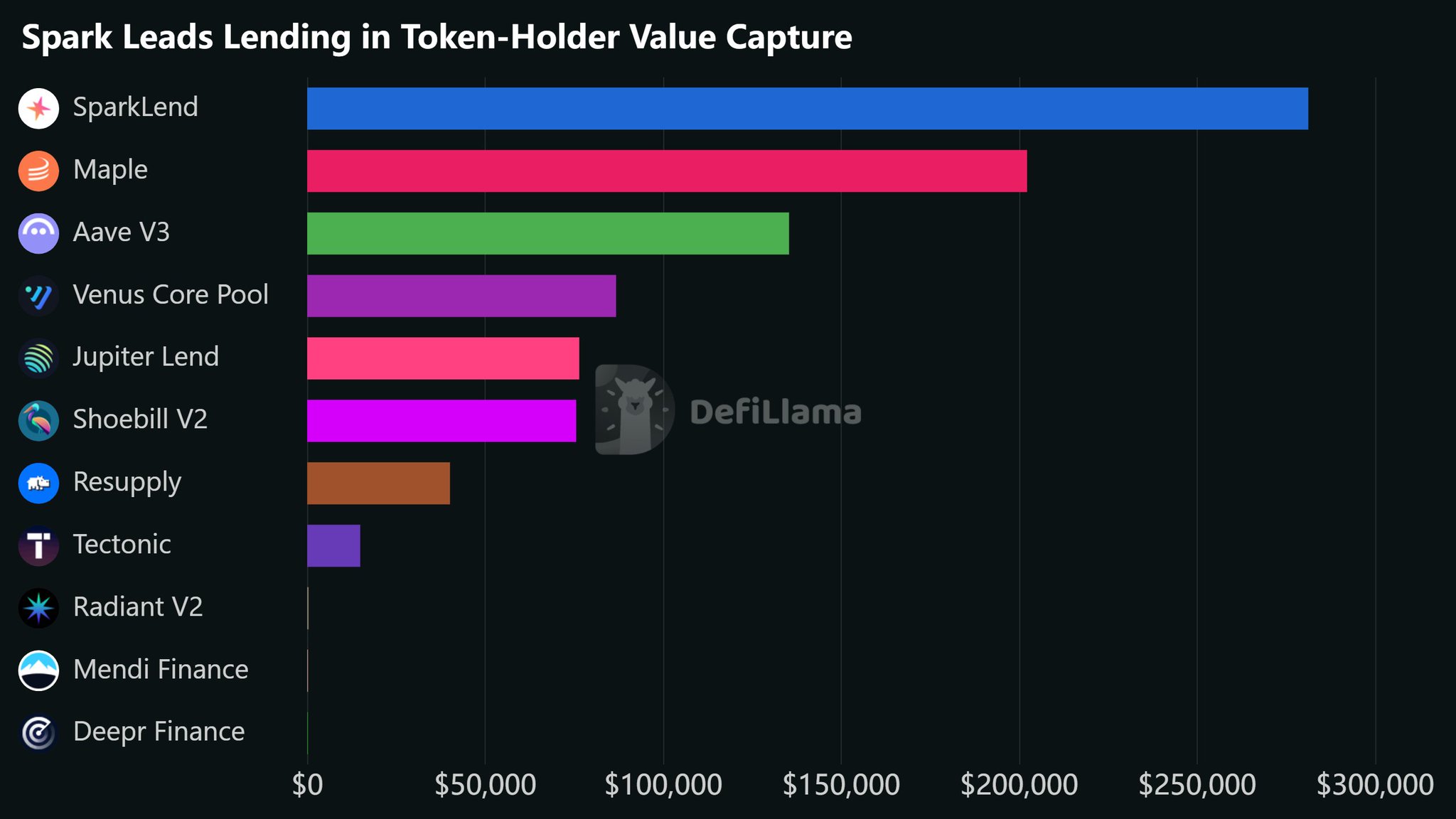

But the sector still has a major weakness: token-holder value capture.

Around 89–90% of lending fees flow to the supply side and other participants, which is expected for a credit market, but it often leaves token holders with little to no direct economic value.

This is where @sparkdotfi becomes interesting.

SparkLend is not just one of the top 10 lending protocols by revenue; it also ranks 1st among tracked lending protocols by 30-day holder revenue, with $281K attributed to SPK buybacks.

That is one of the clearest attempts to convert lending activity and accumulated surplus into visible token-holder value.

The next question is whether that model is sustainable as its $35M buyback program scales.

Thank you @0xTakeProfits and @NexusDataLabs for the priviledge of contributing to this issue

More below ↓