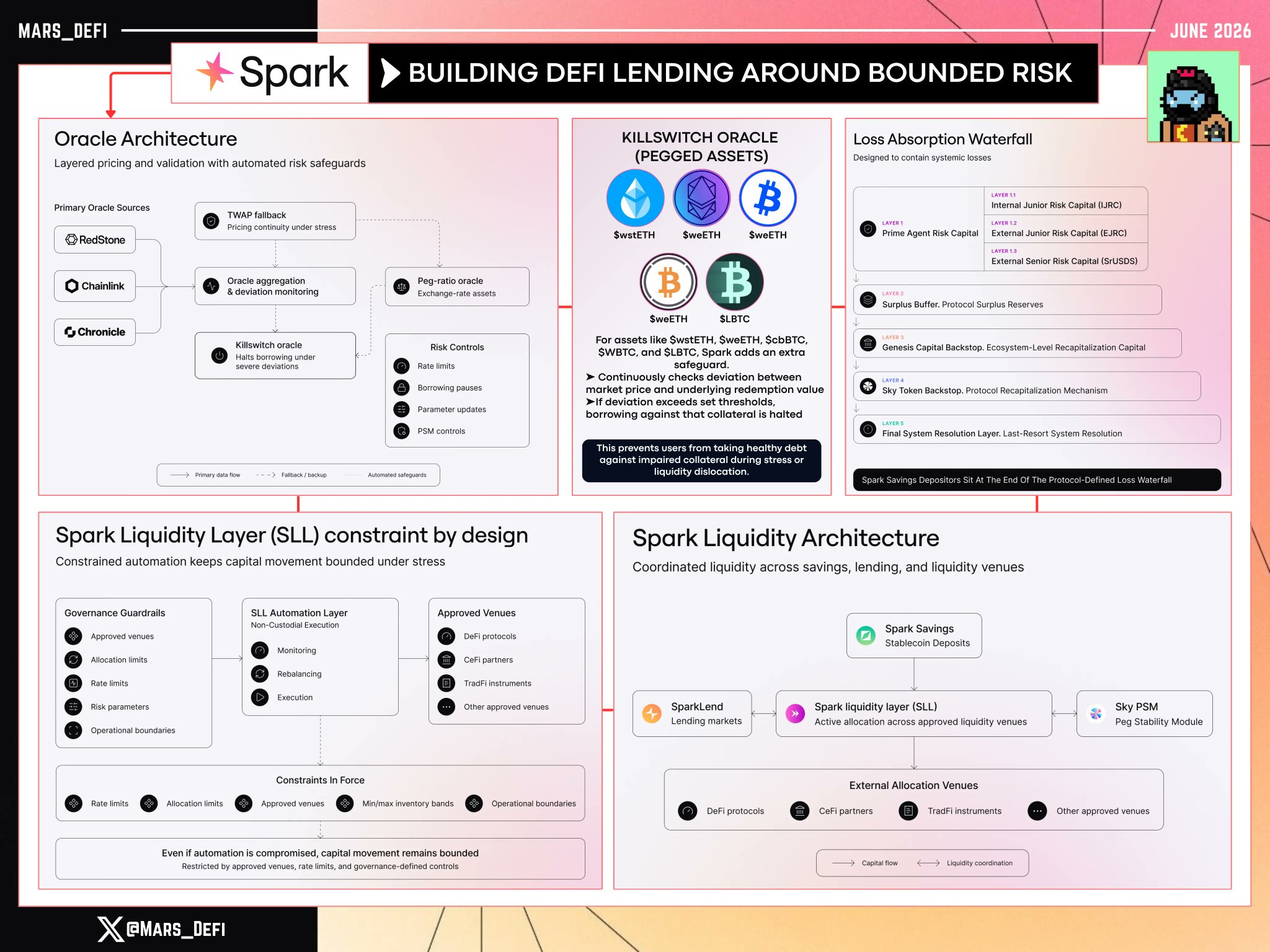

Most lending markets optimize for liquidity and capital efficiency first, then try to manage risk after the fact while @sparkdotfi ’s security/risk framework is one of the better examples of where DeFi lending is heading.

The whole architecture is built around bounded risk, controlled capital movement, layered loss absorption, oracle redundancy, and stress-response mechanisms.

Here’s how Spark does it.

—

Spark keeps a deliberately narrow collateral set, which reduces exposure to fragmented liquidity, weak redemption assumptions, and long-tail collateral risk.

Instead of trying to list every possible asset, it prioritizes predictable liquidation behavior and deeper market structure during stress.

For assets with more unique or chain-specific risks, Spark uses isolated markets. That means risk can be priced more precisely per collateral type, and a single collateral issue does not automatically contaminate the broader pool.

—

The oracle setup is also important.

Spark uses a three-oracle median system drawing from @redstone_defi , @chainlink , and @ChronicleLabs oracle.

When all three return valid prices, the median is used. If only two valid sources are available, the average is used, with fallback logic under degraded conditions.

That reduces dependency on any single oracle provider.

For pegged or exchange-rate assets like $wstETH, $weETH, $cbBTC, $WBTC, and $LBTC, Spark adds another layer through a killswitch oracle.

• This continuously checks whether market pricing is diverging from the underlying exchange-rate or redemption value.

• If deviation passes predefined thresholds, Spark can halt new borrowing against that collateral.

That is a very important safeguard because it prevents users from borrowing healthy debt against impaired collateral during periods of stress, liquidity fragmentation, or pricing dislocation.

—

The liquidity architecture is another strong part of the design.

Spark’s Liquidity Layer is not just idle capital sitting passively in a pool. It coordinates liquidity across Spark Savings, SparkLend, the Sky PSM, and other approved venues.

But the key part is that this liquidity movement is constrained by design.

All venues must be pre‑approved by governance. Capital movement is subject to;

• allocation limits

• rate limits

• min/max inventory bands

• risk parameters

• operational boundaries

Spark’s framework is built around controlled risk, not unlimited automation.

Capital can only move through approved venues, rate limits, allocation limits, and governance‑defined boundaries. So even if automation fails, the damage is contained.

The same idea applies to losses.

Before depositors are affected, losses pass through multiple buffers: risk capital, surplus buffer, Genesis Backstop, SKY backstop, and final resolution.

Spark Savings also has 1:1 USDS backing, liquidity buffers, fast withdrawal routing, real-time transparency, Credora risk reviews, and limited bridge exposure.

—

Overall, the theme is simple:

Spark is not just chasing higher yields.

It is building DeFi credit infrastructure around constrained liquidity, layered protection, and limited blast radius.