Crypto cards have successfully solved spending, but privacy is emerging as the next competitive battleground.

For the last two years, the market competed on cashback, yield, UX, and self-custody, but the @ether_fi incident exposed a new challenge: protecting user financial data.

Here's what's actually happening:

—

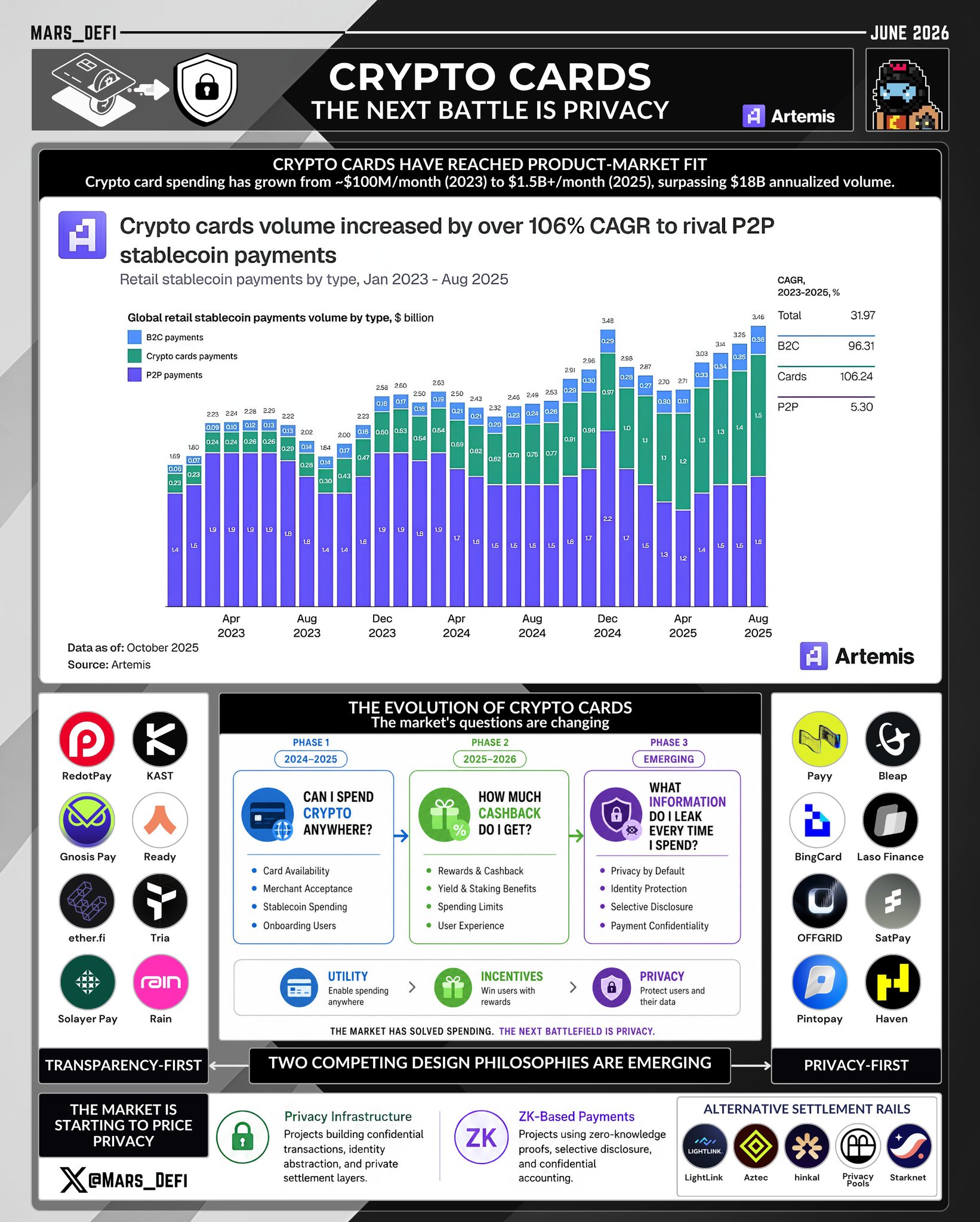

● Crypto Cards Have Officially Reached Product-Market Fit

Crypto cards have evolved from a niche experiment into a legitimate payment category, with monthly spending volume growing from roughly $100M in early 2023 to more than $1.5B by late 2025.

• Cashback rewards

• Yield-bearing balances

• Higher spending limits

• Geographic expansion

• Better user experience

Over the last two years, competition has centered around making stablecoin payments feel as seamless as traditional fintech and neobank experiences.

Today, the category generates more than $18B in annualized spending volume, showing that the industry has largely solved the "Can people spend crypto?" problem.

—

● The Conversation Around Crypto Cards Is Changing

As the sector matures, users are no longer asking whether they can spend crypto, but what they sacrifice every time they do.

• Phase 1 (2024–2025): "Can I spend crypto anywhere?"

• Phase 2 (2025–2026): "How much cashback do I get?"

• Phase 3 (Emerging): "What information do I leak every time I spend?"

This shift reflects a broader realization that what works for DeFi does not necessarily work for consumer payments.

—

● The Hidden Tradeoff Behind Self-Custodial Payments

Users thought they were getting self-custody and financial freedom, but often received self-custody and radical transparency.

The debate is shifting from custodial vs self-custodial to public vs private settlement, and ultimately from wallet ownership to data ownership.

—

● Two Competing Design Philosophies Are Emerging

As the market shifts toward privacy, crypto payments are beginning to split into transparency-first and privacy-first settlement models.

• Transparency-First

Most existing card infrastructure is built around public ledgers, where transactions remain auditable, verifiable, and visible on-chain.

This model is represented by @RedotPay, @KASTxyz, @ether_fi, @useTria, @gnosispay, @ready_co, @Solayer_Pay, @raincards, and other cards built on public settlement rails.

• Privacy-First

A newer category is emerging around private-by-default payments and selective disclosure.

Projects exploring this direction include @payy_link, @BleapApp, @cryptoBingCard, @LasoFinance, @offgridcash, @sat_pay, @pintopay_me, and @Haven_Hn_.

—

● The Market Is Starting To Price Privacy

If this trend continues, capital may increasingly flow toward privacy infrastructure, ZK payments, and alternative settlement rails.

• Privacy Infrastructure: Projects building confidential transactions, identity abstraction, and private settlement layers.

• ZK-Based Payments: Projects using zero-knowledge proofs, selective disclosure, and confidential accounting.

• Alternative Settlement Rails: @LightLinkChain, @aztecnetwork, @hinkal_protocol, @0xprivacypools, and @Starknet privacy initiatives.

AI has dramatically reduced the cost of wallet clustering, identity discovery, and behavioral analysis, accelerating this shift.

—

Today, crypto cards compete on rewards, yield, availability, and fees; tomorrow, they may compete on privacy and identity protection.

Users are beginning to evaluate not just what they earn, but what they reveal.

Crypto payments have largely solved accessibility and rewards; the next battleground is infrastructure that combines self-custody, compliance, and privacy.