Protocols tend to explain their risk model after something fails.

@sparkdotfi publishing its full risk playbook now feels like a pretty confident move, especially while the market is still dealing with exploits and shutdowns.

Basically, when a loan goes bad and someone has to cover it, depositors are usually the first ones to take a loss. Spark made it so they're the last in line during a scenario like this.

It's a meaningful design choice for their entire community.

Let's see how they handle these worst-case scenarios in-depth ↓

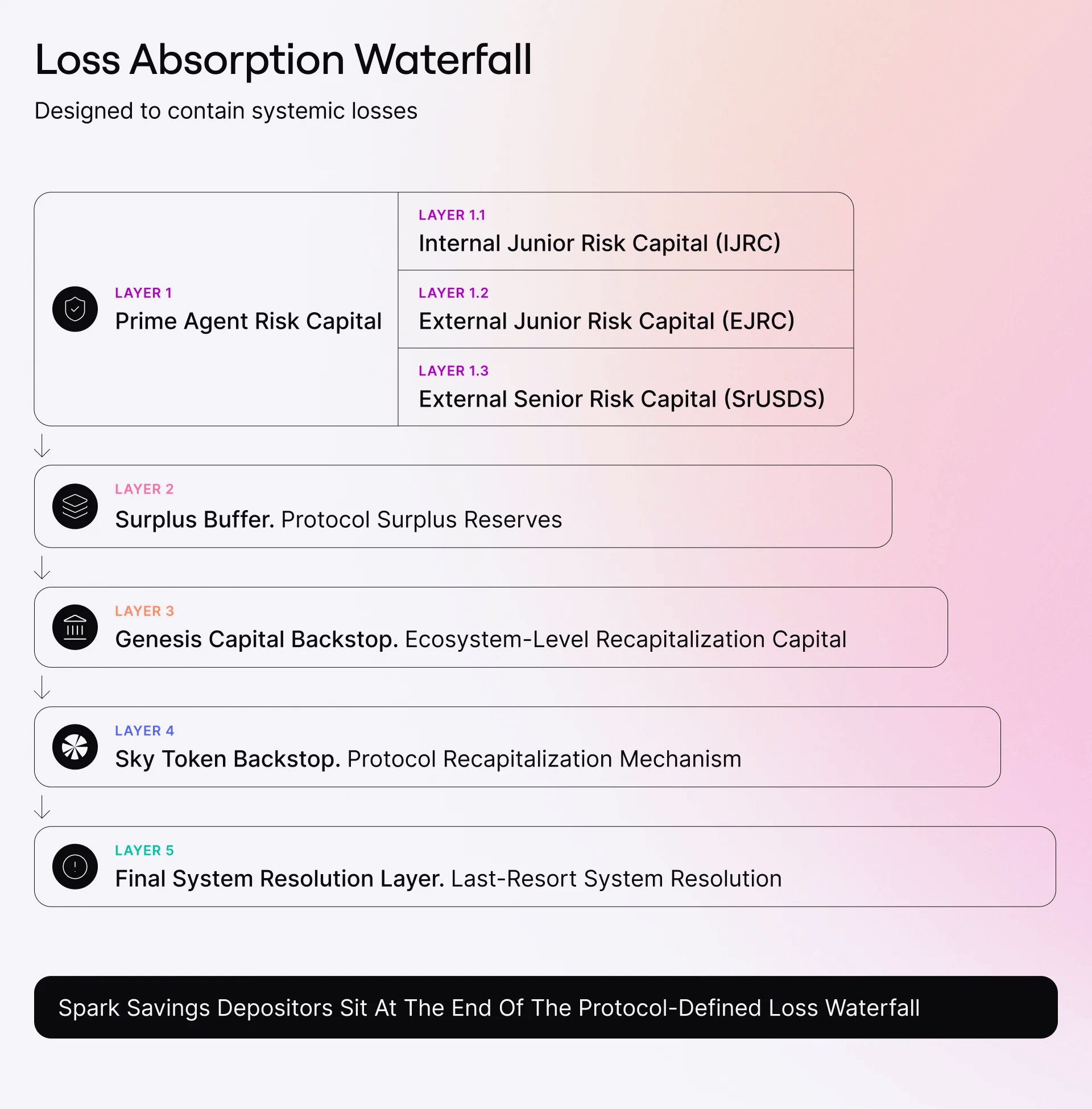

1/ Loss absorption model

Losses are covered in this order before depositors are affected:

→ Spark's own reserves

→ Outside investors

→ Protocol's savings

→ A shared safety fund across the wider Sky Ecosystem

→ Newly minted SKY (as a final backstop)

For user deposits to take a hit, all of those protection layers would have to be wiped out first, and that's highly unlikely.

Spark is also adding more protection for depositors.

@SkyEcosystem recently put $150M into a dedicated reserve instead of using it for SKY buybacks, giving Spark another buffer before user deposits start getting affected in a worst-case scenario.

A security model with so many defensive layers for users is a pretty rare sight in DeFi, at least for me.

2/ Asset containment

All of these protection layers are a backup plan. Spark's design is mostly about making sure it never has to use them.

A lot of its yield comes from moving idle stablecoins around, and most of that is automated. So the obvious question is, what happens if someone hijacks it?

The automation can only send funds to pre-approved places, and only in limited amounts. So even if someone somehow got control, they wouldn’t be able to drain the whole system. They’d be stuck moving tiny amounts into the same audited venues Spark already uses.

The same approach applies to bridge exposure, which is one of the most common sources of major crypto exploits.

Spark deliberately caps its bridge exposure at around $2M, even though the protocol itself holds billions.

3/ Pricing without single points of failure

The other place lending protocols usually break is pricing.

Most lending hacks are just fake value attacks. They make collateral look more valuable than it is and borrow real assets against it, leaving the protocol stuck with holding the worthless asset.

Spark makes this process super difficult by:

→ Not relying on one price source

→ Adding extra protection around assets that are more likely to drift from their expected value (staked ETH, wrapped Bitcoin)

That’s the whole point of this pricing system: bad collateral shouldn’t be allowed to turn into debt for the rest of the users.

4/ A live stress test

Risk frameworks sound nice on paper. But the real question is what happens when they get tested in a real scenario.

Earlier this year, rsETH ran into serious trouble after a lot of lending markets had already accepted it as collateral. Spark had cut rsETH months before the trouble started, so the damage never reached its system.

That was well-timed risk management. Over the past year, Spark has been steadily removing older, smaller, and lower-usage markets.

The whole thing comes down to one word: containment.

When something breaks (and in crypto, something always eventually does), the damage should be contained as much as possible.

The infrastructure underneath Spark has run for the better part of a decade without a single known smart contract exploit, which is quite rare in DeFi.

On top of that, the Spark Savings vaults are independently rated by Credora.

Of course, none of this makes Spark unbreakable.

But after watching so many protocols run with weak risk plans, or no real plan at all, I respect how seriously Spark seems to take this side of the product.

Other protocols should take notes.